Nanoco Group Plc - US trial against Samsung to commence 12th September, compelling risk / reward

Timely special situation investment idea

Listed on London Stock Exchange, Main Market - ticker NANO.

Share Price £0.425 / 42.5p

Market Cap. £137m

Introduction

This is a special situation investment, based on a patent infringement case that Nanoco have brought against Samsung, with the US trial to commence 12th September. Arguably the most interesting period for risk / reward is pre-trial so this idea is very timely. Nanoco’s operational business is the research, development, & production / licensing of nanomaterials for use in commercial applications - however they are yet to secure any production / licensing for a live product, hence minimal revenue. I will be focusing on the legal case against Samsung, settlement of which could be transformational for the company and shareholder value.

Background of dispute with Samsung

Nanoco was formed from a university research group (from the University of Manchester, in England), and has been researching nanoparticle and quantum dot technology for a long time, with the research & manufacturing headquarters being established in 2001.

Nanoco developed quantum dots for display purposes (e.g. high end premium TV’s), which were importantly free from heavy metals which bring health risks such as cadmium. The quantum dots are referred to as cadmium free quantum dots (CFQD). Importantly they also developed a method to scale up from lab to volume production.

Back in 2010 Samsung engaged with Nanoco to evaluate the quantum dot technology, and were provided samples by Nanoco. Samsung did not licence the technology, but went on to debut a TV with quantum dots at Consumer Electronics Show 2015. Further Samsung launched a TV with cadmium-free quantum dots in 2017 branded “QLED”. Nanoco believes Samsung has wilfully infringed a number of patents in the production of their QLED TV’s.

This 2017 article by Samsung, declares the development of CFQD technology for QLED TV’s as a breakthrough achievement by Samsung, crediting Dr Eunjoo Jang as the architect behind it.

However, you can see in this email from 2006 Dr Jang asking Nanoco about their cadmium free quantum dots - this is taken from the IPR materials, but there are many public documents from the PTAB IPR and the ongoing Trial available to review.

Legal progress in USA

Key steps achieved so far in the US legal process are as follows:

Obtained legal funding such that they can pursue the case, even though they have limited cash resources. The funder is not disclosed, but presumably would have done significant due diligence before agreeing to back the case. The funder will take a cut if successful, which would leave Nanoco with 50% of a modest trial award, up to 80% of a larger award.

Trial process:

Feb. 2020 - filed complaint in the Eastern District of Texas (can follow the case on PACER, with CIVIL DOCKET FOR CASE #: 2:20-cv-00038-JRG).

Mar. 2021 - Markman hearing, Nanoco won 4 of 5 patents.

August 2022 - Samsung attempted to change the court agreed definition of a Molecular Cluster Compound (MCC), and this was rejected.

Trial stayed while IPR at PTAB is held (see below), the positive PTAB outcome showing validity of the patents allows the Trial to focus on the alleged wilful infringement, and damages.

Aug. 2022 - Pre-Trial conference held, Nanoco damages models & expert testimony preserved. Nanoco have focused the trial strategy on green quantum dots, hence judge has agreed to issue summary judgement of non-infringement with regard to red quantum dots.

Patent Trial and Appeal Board (PTAB) process:

May 2021 - Inter partes review (IPR) instituted to determine validity of 47 claims within the 5 patents.

May 2022 - PTAB ruled in Nanoco’s favour in respect of all 47 claims. This was a very positive step, confirming validity of the patents.

Note that Samsung are appealing the PTAB outcome, however this is not delaying the trial going ahead.

The PTAB outcome was a material positive (shares traded at c. 27p prior to outcome being announced, having been closer to 20p when the PTAB oral hearing was heard in February 2022), and along with further positive updates (legal rejection of change to MCC definition, work package for European customer, oversubscribed fundraise), have given the shares momentum to now stand at c. 42p.

Launch of Legal Action in Germany

The USA represents approximately 35% of Samsung’s QD TV sales (as estimated by Nanoco), however Nanoco have a worldwide patent portfolio, and will be looking to either reach a global settlement with Samsung, or take action in various other geographies if successful in the USA.

They have just recently announced (23rd August) that they have filed a funded law suit in Germany, which is one of the largest European markets for high-end TV’s. I think this is laying the groundwork to increase the pressure on Samsung, and particularly if they are successful in the upcoming US trial. There is a risk with the US trial that Samsung appeal the outcome, and attempt to drag out actually paying damages for a number of years. However, in Germany it is much more common to grant an injunction prohibiting sale of infringing products, if Nanoco can win the US trial it is very possible such an injunction could be granted in Germany. This would be a significant real world impact to Samsung’s business, and help push Samsung to agree to a settlement.

Damages / Settlement Possibilities

If Nanoco win the case, it is very difficult to accurately predict damages. I will therefore suggest some figures that people can play with. Note if successful in the US trial this will award damages for historical US sales, and may or may not specify a royalty for future US sales - it will not include anything for non-US sales. However, if a settlement is reached with Samsung, my understanding is this would likely be a single amount to cover worldwide historical and future sales

Worldwide Samsung QLED TV sales, per Omdia:

Note - current year and future year TV sales are very important.

Reference: pulsenews link

Damages per TV - I would recommend reviewing the earnings call transcript from 3rd Nov. 2021 where CEO Brian Tenner talks at length about damages (available on TIKR). There are various damages models:

Nanoco would contend that their IP enabled the entire device (alas the CFQD’s are very key to a premium QLED TV), and therefore you could reference the value of the entire TV (note the average retail device sales price was typically $2,000 - $2,500).

Another model is to consider the value of key components, given how important the CFQD’s are to the picture quality (and for health / safety), this would also be an attractive model for Nanoco. Note that the Samsung QD TV’s retailed for approximately $1,000 more than non QD TV’s.

Lowest model is to use individual component value, i.e. of the QD film itself. I think there is a risk that historical discussions between Samsung & Nanoco may have referenced modest sales or royalty rates that may now be used to limit the damages awarded. I don’t know what these figures would be, but note that Edison estimated a royalty at $14.4 - 18.0 per TV, and Turner Pope Investments (TPI) estimated a low-end royalty in the range of $8 - 12 per TV. Both Edison and TPI “research” is paid for by Nanoco, so although the estimates will be presented as their own, you could wonder if Nanoco would have steered them a bit.

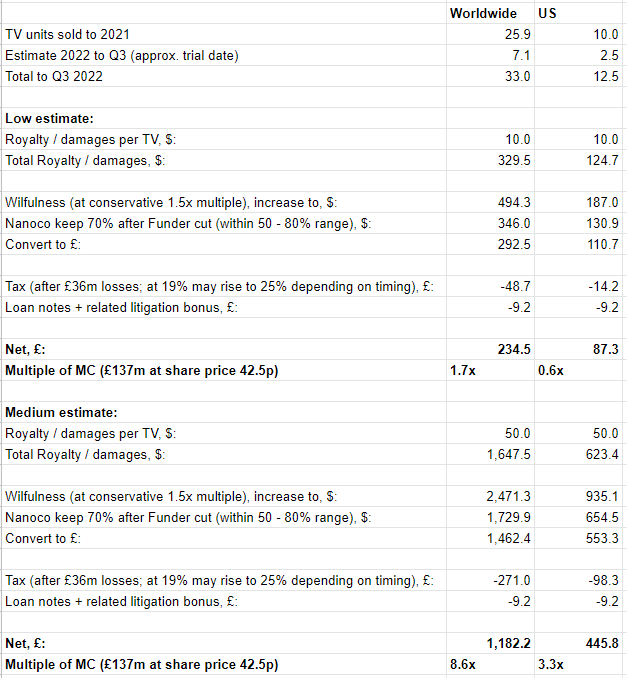

For simplicity assume a low estimate of $10 per TV, and medium estimate of $50 per TV being 5% of the approx. $1,000 increase in value of a QD TV vs non QD TV.

Nanoco are alleging wilful infringement, and I would note the collaboration between the parties before Samsung decided to produce the quantum dots without paying Nanoco anything for the IP. If successful, this can result in a wilfulness multiplier being applied by the US judge of up to 3x, however I have used 1.5x which may be more realistic.

See below for Low & Medium estimates for royalty / damages amounts to approx. trial date Q3 2022, note the current market capitalisation is only £137m:

The above figures do not include future years which are very significant given the 2021 run-rate of sales, and expectations per Brian Tennor 3rd Nov. 2021 transcript “Future sales are likely to be larger because the rate of sale of QD TVs is growing. And you then may have the kick on benefit of generation 2 QD TVs.” If we assume annual TV sales of 10m, just slightly higher than 2021, this would produce a gross yearly royalty amount of $100m at the low estimate ($10 / TV), and $500m at the medium estimate ($50 / TV). The last of the 4 core quantum dot patents expires in early 2028, with another patent out to 2035 (I assume this is the ‘068 patent) - however as part of narrowing the case pre-trial Nanoco have withdrawn claims for the ‘068 & ‘557 patents. I am not sure exactly which of the 4 core quantum dot patents has the last expiry date, but if we assume one of those remaining expires in early 2028 this provides for c. 5 years further coverage. Simply taking 5x the low estimate above is $500m, or 5x the medium estimate is $2,500m.

Operational Business

As can be seen from the saga with Samsung, Nanoco are very dependent on an end product being produced and sold to consumers that integrates their technology, and being paid for it.

Operationally they are focused on supplying quantum dots for infra-red sensing opportunities, they are working with 5 different customers and 8 distinct products, but it is not yet clear if any will move in to production or not. The expectation is that in H2 CY 2022 they will have visibility as to whether one of these customers will move into live production in CY 2023 or not.

I don’t think the company has confirmed, but Edison have inferred that Nanoco’s “important European electronics customer” is ST Microelectronics. They also suggest that if an end customer of ST Microelectronics were to deploy the sensing application in a key mobile phone handset this could generate £15-20m of annual revenue to Nanoco.

If they can get real production orders (or agreed royalties) this part of the business could have real value, but I would not have any confidence in ascribing it significant value until they achieve this.

Financial Situation

The (expensive) litigation process is funded by a third party, and the company has done well at cutting costs in order to maximise their cash runway, further they raised £5.4m in an equity fundraise in June 2022 at 37p / share. As such they have a cash runway to CY 2025 - far past the iminent US trial (although appeals may follow), and it’s also possible they will have real production revenues prior to this point.

Cash (unaudited, as do not have audited FY results yet) at July 2022 £6.8m, debt at half year January 2022 £3.7m. For HY to Jan. 2022 cash burn was £0.3m / month. Note a “major” work package for the European electronics customer was signed in June 2022 which helps to support the cash runway (stated by company in August 2022 to extend to CY 2025).

Downside & Upside

Pre-trial period:

Prior to the trial commencing 12th Sept. I would view the downside as quite limited. Given most of the value ascribed currently relates to their prospects against Samsung, the legal developments to date have generally been very positive, and we have now passed the pre-trial conference point.

There is a real possibility that Samsung decide to make an acceptable settlement offer prior to trial. This would likely be a worldwide settlement agreement for all past & future royalties. This would mean they could avoid the risk of the jury deciding against them and possibly awarding a high amount per TV, and then also be exposed to possibly having an injunction stopping them selling QLED TV’s in Germany shortly afterwards.

At trial:

Although it appears Nanoco are in a strong position going to trial, we don’t know what will come out during the trial process, and ultimately they could lose. If this happened I would ascribe minimal value to the operating business at this point, so would estimate downside at c. 90%. This may be harsh, but they have not yet secured production orders for their sensing applications.

For upside, please see above the Damages / Settlement section, albeit the US trial itself will only award damages for US historic sales, and possibly set a royalty for US future sales.

Therefore, I view the risk / reward as incredibly compelling during this pre-trial period where a substantial settlement could be announced which would be transformational for the company. Once the trial starts it becomes much more binary, and while still interesting I would likely look to size the position much smaller.

Other points to note

Their largest shareholder is Lombard Odier Asset Management at c. 23%. They have historically been supportive, including subscribing for loan notes. More recently they have been reducing their holding, it should be noted the share price has increased substantially this year, and I don’t know the driver for their recent transactions i.e. portfolio / risk management vs change in view.

Richard Griffiths (/ related entities) was historically a large shareholder, and also supported the loan notes, however he has recently sold down his shareholding to below reportable threshold.

Disclosure

Long Nanoco Group Plc at time of posting.

This post is not investment advice.